Functional Neurological Disorder ICD-10 Codes

Published November 2, 2023

Download for free today

Download now

Download for free today

Download nowInsurance reimbursement rates for CPT codes in the mental health field affect how practitioners set their rates. Whether they’re paneled with an insurance company or see self-pay clients only, there can be a lot of mystery when it comes to deciphering commonly used CPT codes.

To shed light on what earning potential looks like for therapists paneled with insurance companies, SimplePractice examined reimbursement rates for three of the most common Current Procedural Terminology codes (CPTⓇ codes) used by behavioral health practices. These codes are 90837, 90834, and 90791, and were used for 2.2 million appointments from January 1st through August 8th, 2021.

The results showed that payment from insurance companies for these mental health CPTⓇ codes drastically vary and may prove financially limiting for clinicians if they’re paneled with just one insurance plan.

This article examines everything from insurance reimbursement rates by profession, to demystifying commonly used CPT codes. You can also learn about the median reimbursement rates from insurance companies across the US, and how you can set your rate depending on what state you’re licensed in.

In 2008, the federal parity law was passed, which required most insurance companies to cover services for mental health, behavioral health, and substance use disorders at a comparable rate to physical health coverage. However, as with any medical condition, insurance companies have the final say in determining whether or not a treatment for an individual’s condition is a “medical necessity.”

To better understand the state of insurance within the mental health industry and shed light on what earning potential looks like for therapists, SimplePractice examined reimbursement rates for three of the most common Current Procedural Terminology codes (CPT® codes) used by behavioral health practices. Codes 90837, 90834, and 90791 were used for 2.2 million appointments from January 1st through August 8th, 2021.

The results showed that payment from insurance companies for these CPT® codes drastically vary and can prove to be financially limiting for clinicians if they’re paneled with just one insurance payer.

Despite the low reimbursement rates from insurance companies, a considerable number of clinicians opt to accept insurance for their practice. While there may be a number of reasons for this, practitioners seem to recognize that the benefits of being paneled with insurance can outweigh the setbacks.

If you ask a therapist—or any clinician for that matter—about the credentialing process to panel with insurance, you’ll most likely get an eye roll. Yet, more practitioners continue to panel with insurance companies despite the tedious process. How does this make sense?

For starters, many clinicians find that being paneled with insurance is a great way to grow their caseload at a faster rate. Whether they’re just beginning their career or looking to find more clients, being part of a network and accepting insurance allows for more business growth opportunities at a quicker pace than trying to find self-pay clients.

Dr. Ben Caldwell states, “Many clinicians want stability of income, and to not have to market themselves. Paneling with insurance allows them to focus on clinical care rather than spending time on marketing.”

Dustin Alipour, Lead Insurance Specialist at SimplePractice, agrees. “With a self-pay practice, there’s a lot of ‘selling yourself’ and ‘self marketing’ you have to do. This includes marketing your practice, building a brand, networking, and more. However, if you get paneled with an insurance payer, these are all things you may not have to worry about. Insurance companies will actively refer clients to you via their network directory. Working with insurance allows you to build your practice a lot faster,” he says.

One of the biggest appeals to offering insurance is providing care to clients who may not be able to afford mental health services. Because of this, more people tend to start their therapist search by seeing what clinician is covered under their insurance plan. While it never hurts to set up an online presence where therapy seekers can search for clinicians in their area, one of the best ways to start making a steady income is to panel with insurance.

Alipour also mentions, “Insurance has a larger barrier to entry. However, once you’re in, you’re in. With self-pay, it’s always going to take a lot of work on your part until you get so well known that your clients start referring other clients to you—and even that is not a guarantee.”

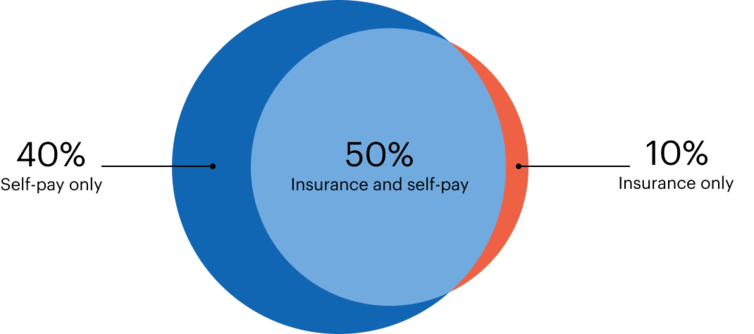

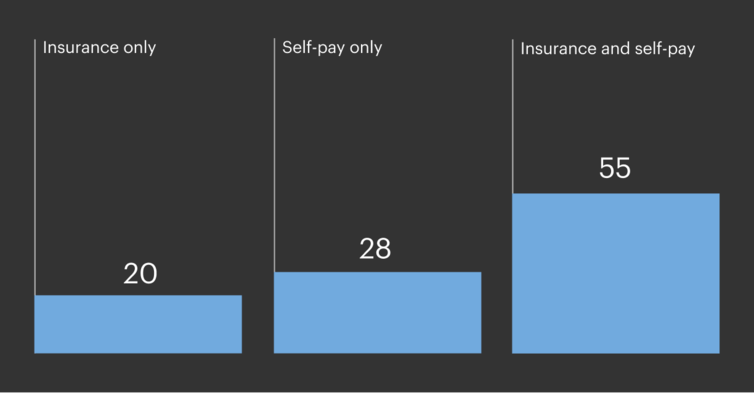

SimplePractice examined the different appointment types of clinicians during the month of August in 2021. The results showed that 60% accept insurance for their practice, of which 50% also accept self-pay. The 10% difference is made up of clinicians who only accept insurance appointments.

Percentage of clinicians per billing strategy (August 2021)

N=116,000, Source: SimplePractice, 2021 CPT® Code Study

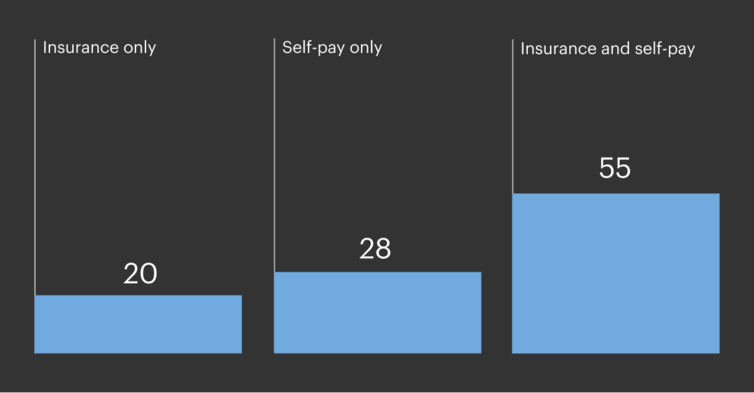

At a closer look, the median number of appointments a clinician has with insurance-only clients is quite small, with a low average of only 20 appointments a month.

Average number of appointments per billing type (August 2021)

N=116,000, Source: SimplePractice, 2021 CPT® Code Study

While clinicians who accept insurance-only appointments may be in the minority, there could be a number of reasons for this—they might be part-time or just beginning their practice. It’s also possible that clinicians who accept both self-pay and insurance might already have an established practice, but are still looking to grow their caseload.

A common myth is that practitioners need to do the entire credentialing process on their own. This, in fact, is not true. Some practitioners seek resources to walk them through the credentialing steps, while others choose to hire a billing specialist or someone well-versed in the credentialing process.

While this can be a time-saving solution, clinicians may start to run into problems when they hire outside help. Usually these are minor issues such as the third party misspelling the practitioner’s name or putting the wrong birth year down. While these are easy fixes, setbacks like these can drastically slow down the process.

The world of insurance is constantly changing and is largely not taught in schools. As many practitioners have discovered first-hand, it can be challenging to understand and solve insurance issues when they’re not well-versed in insurance terms, the billing process, or CPT® codes.

Despite the practitioner getting approved for a list of billable CPT® codes, not every client has benefits to cover each service. The first thing a practitioner needs to do when they bring on new clients under insurance is to verify their insurance benefits and check what the client has active coverage for.

In general, therapists should get credentialed in the way that works best for them. For clinicians who use a third party to get paneled, it’s still worth making sure they have a solid understanding of what insurance billing entails, so they’re able to take action if problems arise.

CPT® codes are five digit numerical codes created by the American Medical Association (AMA) to identify a service or procedure by qualified healthcare professionals.

These codes are used to represent the service that was rendered in a standardized manner. Insurance companies all use these same codes to determine how much to reimburse for the session. However, each insurance plan may reimburse at different rates for the same CPT® code.

When the clinician is paneled with an insurance company, the plan provides the clinician with a list of the contracted rate for each service they’re credentialed to render. These contracted rates are specific to each insurance company and contain the list of CPT® codes you may provide.

Each year, the AMA makes updates or changes to CPT® codes that are ready to use on January 1st of the new year. It’s up to the practitioner to make sure they keep track of each year’s updates, so when they bill insurance the right code is being used for reimbursement.

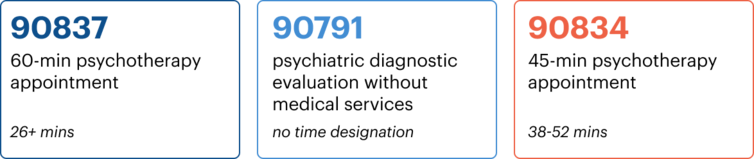

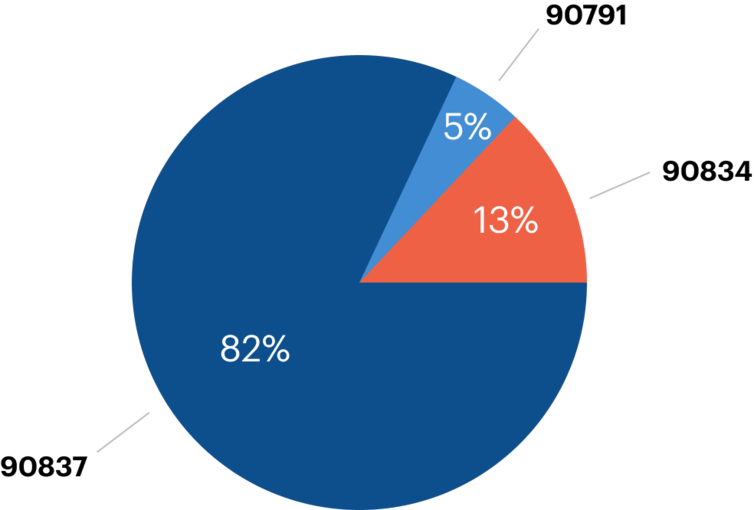

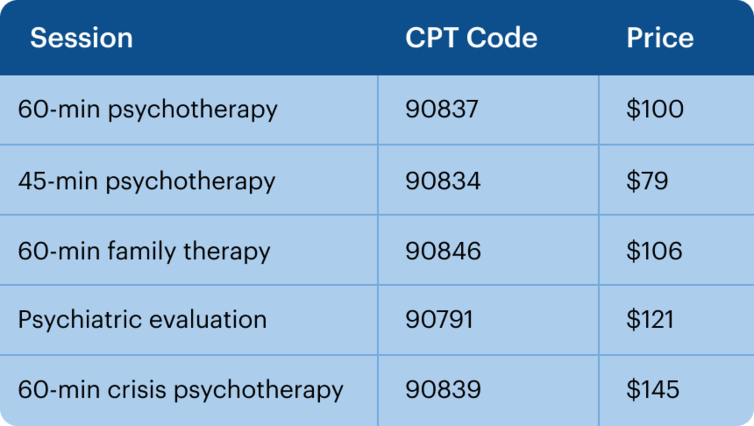

When it comes to CPT® codes, there are three standard codes that are frequently used by clinicians in the behavioral health field or related fields. These are also the three CPT® codes that were primarily focused on in this SimplePractice study.

A closer look indicates that CPT® code 90837 was billed the most, followed by 90834 and then 90791.

Appointments booked per CPT® code (August 2021)

N=116,000, Source: SimplePractice, 2021 CPT® Code Study

The most frequently billed CPT® code in 2021 was 90837. Defined as a 60-minute psychotherapy session, this code can be used for any session 53 minutes and longer. It is not surprising that 90837 is the most frequently billed psychotherapy code across the United States, as an hour-long therapy session is most common among behavioral health therapists.

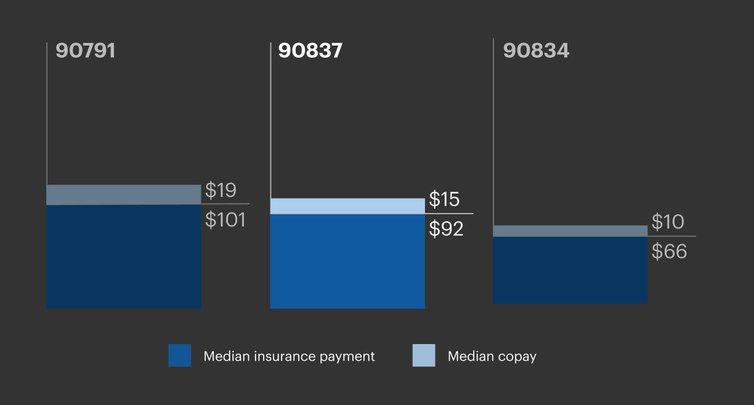

The total median payment was $107—with insurance reimbursing $92 and the client’s copay making up the difference.

National median insurance payment and copay amounts (2021)

N=2,196,977, Source: SimplePractice, 2021 CPT® Code Study

In recent years, there’s been pushback from some insurance companies when it comes to using 90837.

In 2015, letters were sent out by EquiClaim on behalf of Anthem Blue Cross Blue Shield, targeting certain clinicians who were frequently billing 90837. Although the letters were sent out to be informative, there was an implication that therapists might need to provide lengthy medical records if they continued to bill 90837, and could be subject to audits.

Although Anthem Blue Cross Blue Shield apologized for their tone, providers across the country have continued to get similar letters from Blue Cross and other health plans, informing them that they use 90837 more frequently than colleagues, and sometimes asking that the provider contact the Education Team to discuss it.

In this case, if the provider is asked to defend the use of 90837, it is advised that the practitioner lets the insurance company know they understand that:

CPT® code 90837 is often incorrectly used to bill for ongoing couples and family therapy. This may happen for three reasons:

Despite situations like these, practitioners should not avoid using 90837 completely when billing insurance plans for their 60-minute sessions, if that is in fact the service that was provided. Doing so could represent a significant loss of income.

There are certain insurance companies that will use 90837 as an “extended session” rather than the code for routine therapy. In this case, it is advised that you make sure any documentation matches the insurance company’s standards and to follow the plan’s policies. As always, practitioners need to double check their contract with their insurance payer.

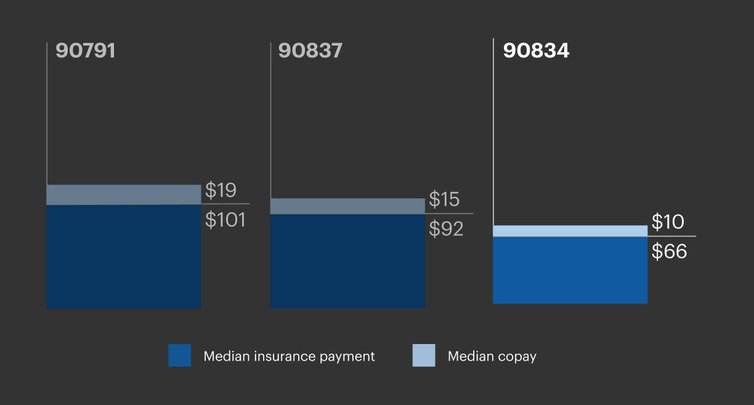

The second most-billed CPT® code in 2021 was 90834—a 45-minute psychotherapy session. CPT® code 90834 covers sessions ranging from 38 minutes to 52 minutes, which means that a clinician will get paid the same amount for a 38-minute session as they would for a 52-minute session.

Although the median total payment for this code is lower than the others, clinicians may benefit from it in the long run. The median total payment is $76, with insurance paying $66 and client’s copay making up the difference.

National median total payment amount (2021)

N=2,196,977, Source: SimplePractice, 2021 CPT® Code Study

National median insurance payment and copay amounts (2021)

N=2,196,977, Source: SimplePractice, 2021 CPT® Code Study

Dr. Ben Caldwell states, “I’ve been saying for a long time that it’s in our best economic interest to have standard appointment lengths that are less than 50 minutes. Even 40 or 45 minute sessions can free up time for a practitioner without impacting their reimbursement rate.”

Even though the median total payment for 90834 is lower than the 90837 and 90791, clinicians can make it up by seeing more clients, or pairing it with self-pay clients. For practitioners who have just started in the field—or have an urgency to grow their client base—they could take on more appointments in a day and still average the same amount of money as they would by offering fewer 60-minute sessions.

For example, if a practitioner is paid the median rate of $107 for five 60-minute sessions, they would receive $535 for 300 minutes. Compare this to a practitioner who does seven 40-minute sessions a day, they would get $532 for 280 minutes.

If clinicians bill 90834 and structure their appointments using this method, it would allow them to work less hours but see more clients without losing a significant amount of income.

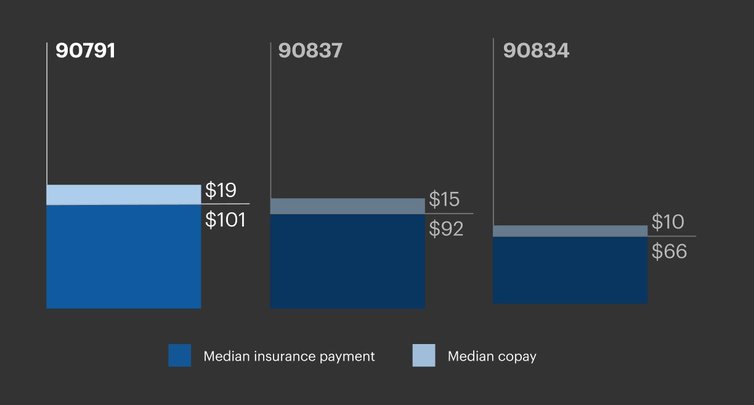

CPT® code 90791—psychiatric diagnostic evaluation without medical services—is the least commonly billed code when compared to 90837 and 90834. Even though 90791 can typically only be used once per customer for the very first session, clinicians tend to skip over it and go straight to billing 90837 or 90834.

This is a common mistake that practitioners make, and as a result, they end up missing out on the benefits of 90791.

First of all, the reimbursement rate for 90791 is almost always higher than 90837 and 90834. The median total payment for billing 90791 was $120. Out of that $120, insurance reimbursed $101, with the client’s copay making up the difference.

National median insurance payment and copay amounts (2021)

N=2,196,977, Source: SimplePractice, 2021 CPT® Code Study

Of course, the total payment amount can drastically vary based on the insurance company, the client’s insurance plan, and other factors. However, this data shows that if a clinician is meeting with a client for the first time, it may make the most sense to bill 90791. Knowing this ahead of time can create more accuracy in the billing process, and minimize the chance of a claim being rejected.

Alipour says, “This is one of the main problems I see from clinicians when it comes to CPT® codes. They aren’t aware that the introductory session needs a different CPT® code since it was essentially an ‘onboarding’ appointment and no regular services were provided.”

Furthermore, clients who see couples and families do not realize they should be using this code for their initial intake sessions for the same reasons—it is the accurate code for a first session, and it may reimburse at a higher rate.

In addition to accurately billing the right session and receiving a higher payment for 90791, many insurance companies don’t require preauthorization for this code. If your insurance company doesn’t require preauthorization, this means that you can see as many clients as you want who are in-network without worrying if the insurance payer will accept your treatment.

While CPT® codes 90834, 90837, and 90791 are used the most, there are some lesser known codes that tend to be underutilized or skipped over.

Something to be aware of when billing 90846 is that even though the identified client isn’t present, the session still needs to be centered around the identified client’s illness or condition—not the couple or family. The time range for this code is 26 minutes and above.

Code 90839 is used for appointments that require urgent assessments and examination of the client’s mental state. The definition of a crisis is really left to the therapist’s clinical judgement. However, examples of this may include clients displaying suicidal behavior— or other extreme distress or psychological symptoms—where the therapist may need to mobilize resources to reduce potential trauma. The time range for this code is 30- 74 minutes. For crisis sessions longer than 74 minutes, a 90840 add-on code (crisis psychotherapy, each additional 30 minutes) may need to be added.

Many clinicians tend to overlook these CPT® codes and default to billing 90837 or 90834.

It’s always best practice to double check your fee schedule or ask the insurance company before accepting a client under insurance—in case a session you plan on having isn’t billable.

To better understand if a clinician can make a living with insurance-only clients, SimplePractice examined the number of different appointment types a practitioner has.

A good rule of thumb for clinicians to avoid burnout is to average between five and seven appointments per day, five days a week. However, depending on what their payment situation is (accepting insurance, rate of reimbursement, price for self-pay, etc.) and how many clients they see, the number of appointments per day can vary for each clinician.

Average number of appointments per billing type (August 2021)

N=116,000, Source: SimplePractice, 2021 CPT® Code Study

The median number of appointments an insurance-only clinician has is 20 per month, which is less than half than that of practitioners with insurance and self-pay appointments.

There are a number of reasons this could be the case. For example, these clinicians could be part-time members of a group practice, or they’re just starting out in private practice. Regardless, 20 appointments per month might not be enough for a clinician who is just accepting clients under insurance.

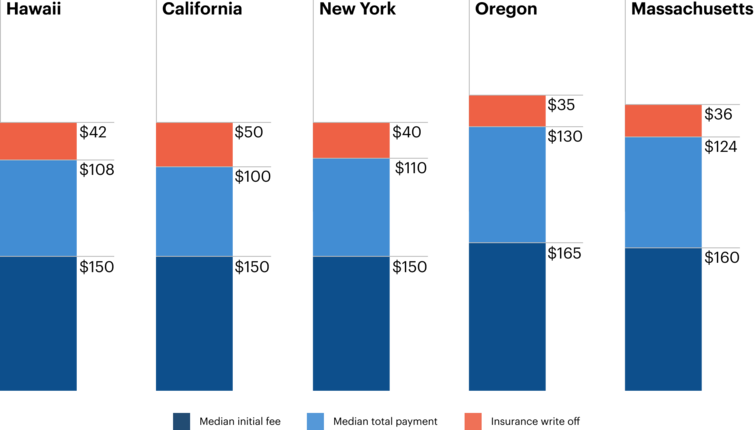

As of 2021, the five most expensive states to live in are Hawaii, California, New York, Oregon, and Massachusetts. The median total payment for CPT® code 90837 falls within the lower hundreds for practitioners within these states.

Insurance payment breakdown in the most expensive states in the US

N=2,196,977, Source: SimplePractice, 2021 CPT® Code Study

In California, the median reimbursement rate for 90837 is $100. However, this is the state- wide median price given that reimbursement rates range from $36 to $344, depending on the clinician’s experience level, license, insurance provider, and city. In addition, the same insurance provider can reimburse different rates within the same state solely based on the location within that state. For example, one provider may reimburse $150 for 90837 in Palo Alto, CA, but only $100 in Los Angeles, CA.

There are many reasons why a clinician could fall into this lower payment bracket within California. This could be due to a lower-paying specialty, their location within California, what degree they have, the insurance provider, and more. Comparatively, a clinician who received a higher total payment of $120 per session, multiplied by 20 appointments a month would make

$28,800 a year.

Despite $120 in total payment being relatively high for California, this still isn’t enough for a clinician to comfortably live off. The same can be said for the other four states that were rated as the most expensive to live in—considering that the median total payment amounts fall around the same number as California.

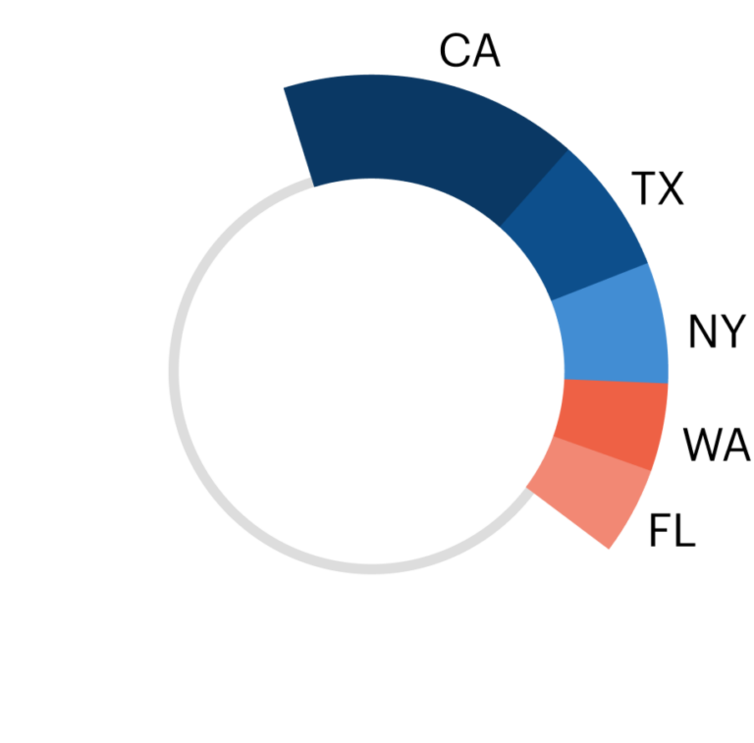

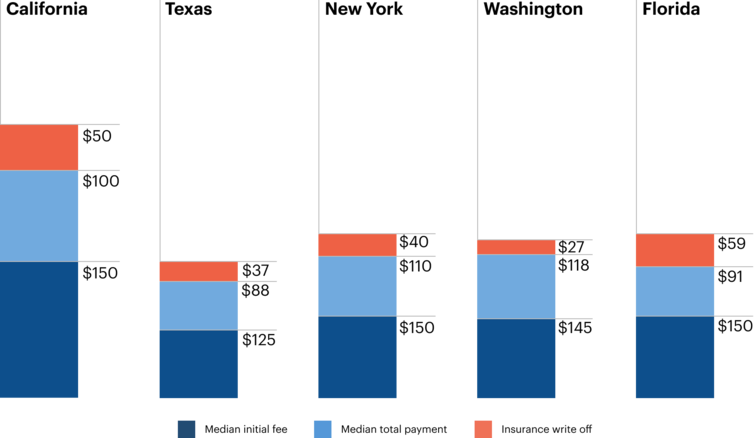

The five states with the most SimplePractice customers are California, Texas, New York, Washington, and Florida. Out of these states, Texas has the lowest median total payment rate at $88 for CPT® code 90837. However, on the scale of most expensive places to live in the US, Texas is number 36—meaning it’s a much more affordable place when compared to California or New York, which are ranked at number two and three, respectively.

States with the most SimplePractice customers

N=2,196,977, Source: SimplePractice, 2021 CPT® Code Study

Insurance payment breakdown in states with the most SimplePractice customers

N=2,196,977, Source: SimplePractice, 2021 CPT® Code Study

If a clinician who is licensed in Texas earns the median total payment rate of $88 for CPT® code 90837 and has 20 appointments per month, they would make $1,760 a month, or $21,120 a year. When compared to California with a median total payment rate of $100 for code 90837 at 20 appointments per month, the total would be $2,000 a month, or $24,000 a year. While the payment totals don’t differ by too much, the value of a dollar can go a lot further in a state like Texas than it can in California.

Clinicians who only accept insurance will either have to increase their caseload, panel with more insurance companies, or start taking private-pay clients to make a comfortable wage that is liveable. Otherwise, it’s not possible to only take insurance to maintain a steady income, especially in the states with the highest cost of living.

Even if you’re not paneled with an insurance company—or are not considering doing so for your practice—insurance rates and CPT® code payments still affect the market rate within your area.

Because so many clinicians begin their careers in private practice by paneling with insurance, the rate that insurance payers set for them ends up influencing the rates practitioners set for themselves the rest of their careers. Clinicians just coming out of school may not know much better, nor have the years of experience to charge more for their services.

Similarly, many new clinicians will join an agency or group, and their payment rate is determined by those groups, who may be paneled with insurance as well.

While this may be the norm, practitioners can generally start seeing self-pay clients at any point of their career. After this, they’re able to get paid a more desirable rate, which in turn is more beneficial to them and their practice.

As most clinicians who are paneled with insurance know, each payer provides a fee schedule for them. This fee schedule is specific to each individual insurance company, and lays out the exact rates the therapist will make for each CPT® code.

The fee schedule rates are based on multiple factors, including the years of experience a clinician has, their licensure, and where they’re located. Unfortunately, not a lot of insurance companies will release their fee schedules or average payments before a clinician has

been contracted. You can try to contact insurance companies to see if they’ll release this information ahead of time, but the answer tends to be “no.”

Once the clinician has reviewed and accepted the fee schedule with their contracted rate for each CPT® code, they need to set a “full fee” for each service they provide in their practice. This full fee should not be the rates that they’ll be reimbursed by the insurance company. In fact, Alipour says, “My biggest advice for clinicians who are setting their rate is to set the rate they want to get paid, not what they’re going to be paid by insurance.” The full fee will be the price that you would charge a private-pay client for that service.

When billing the insurance plan for a session, you should put the full fee on the claim form— not your contracted rate with the plan. This is because insurance payers will re-evaluate and increase their rates for all providers every so often. Alipour says, “When this happens, if you’re only billing exactly what the insurance company paid before the rate increase, they may continue to pay you at the lower rate.”

In addition, setting a higher rate that has been calculated by the market price, years of experience, specialty, and cost of living will help set you up for success when negotiating a potential raise from the insurance payer in the future.

If a clinician decides they also want to take self-pay clients, those clients will pay the full fee the clinician has set, or the clinician can slide their scale to a negotiated rate. Clients have no idea what the insurance company is reimbursing for different types of sessions, so it’s in a clinician’s best interest to set their rate at the price they want to be making. For example, if the insurance company is paying you $50 for 60-minute sessions in Los Angeles, but the average rate for private-pay therapy is $150 for clinicians with the same years of experience and license in Los Angeles, your full fee should match that market rate.

Even though many clinicians worry that setting a different full fee will complicate their billing, Alipour has seen differently. “I see a lot of clinicians set their rate to the reimbursement fee, thinking it will be simpler in the billing process or make their accounting easier to understand. However, it doesn’t make a difference and they end up hurting themselves in the long run.”

Sample fee schedule

Even though many insurance companies won’t release their reimbursement rates until a clinician is contracted, there are still ways to calculate what a competitive rate should be, based on a variety of other factors.

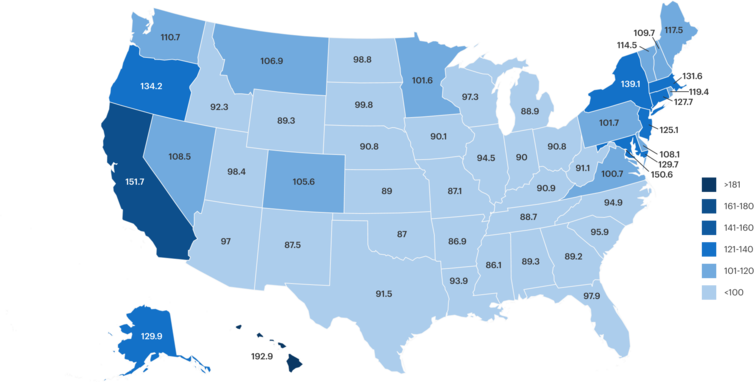

When it comes to the wide range of cost of living in the United States, rates should be based on what state (or states) you’re licensed in, and more specifically what city within that state you plan to serve.

Many insurance companies will pay different rates within the same state based on the city that you live in. For example, one insurance provider may reimburse $200 for CPT® code 90837 in Palo Alto, CA, but only $150 in Los Angeles.

Cost of living index* by state (2021)

N=329.5 million, Source: World Population Review, *The cost of living index is an official metric calculated based on the prices of a representative sample of goods and services in a typical family budget. The index of each state is based on 100, the national average.

One of the main factors when it comes to setting your rate depends on your specialty and license. For example, psychiatrists tend to make much more than a clinical psychologist does. Clinicians who have a masters-level license—such as a clinical social worker, marriage and family therapist, or a licensed professional counselor—typically make less.

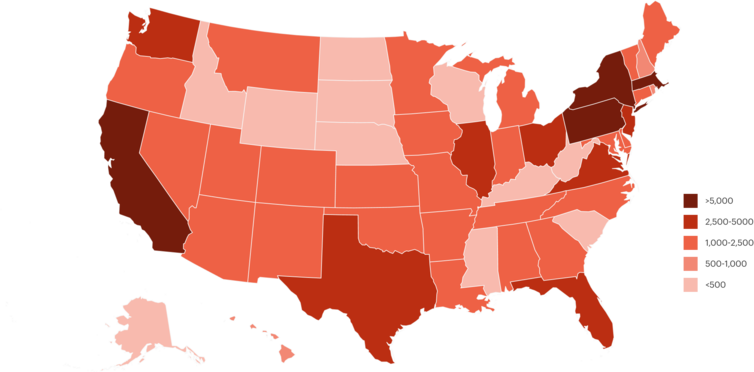

A study done by the American Psychological Association (APA) in 2018 examined all 50 states to find which ones have the most licensed psychologists. Perhaps unsurprisingly, California came out on top with New York trailing close behind. States such as South Dakota, Wyoming, and Alaska had the fewest licensed psychologists.

While this study focused solely on psychologists with doctoral-level degrees, this gives some insight into what the demand might be for behavioral health services in each state, and how your rates can be adjusted accordingly.

Number of active doctorate-level licensed psychologists (2018)

N=102,000, Source: American Psychological Association

On top of regular expenses such as rent, groceries, transportation, and bills, student loans are one of the main financial constraints that psychologists face today.

An APA study found that about 50% of psychology students were paying for their graduate programs with student loans. The study also found that Doctor of Psychology students rack up the most debt, with a median of $50,000 in loans. So when it comes time to determine your rate for services, it’s important to make sure that you can comfortably cover bigger expenses like student loan payments.

It’s a good idea to approach the question of rates from the opposite direction—how much money do you need/want to be making after all your expenses are paid? Once you figure out how much you need to make per month, you can divide this number by the number of sessions you plan to provide that month. This will give you how much you need to charge on average per session to get your desired monthly amount. Don’t forget to allow for missed sessions and vacation/sick days.

While these are standard considerations any clinician should take when setting a rate for their practice, some other things to keep in mind are level of education, different licenses, and years of experience.

Remember—even if you’re only accepting clients through insurance, these are best practices for setting your fee. The same can also be applied if you’re figuring out how to set your rate for private pay, but don’t know where to get started or how to increase your current rate.

To find out what the median total payment amounts are per state, SimplePractice examined appointment types, along with their billing strategy to create a median fee breakdown for CPT® codes 90837, 90834, and 90791.

This data was taken by looking at SimplePractice customers’ billed appointments, filtered by insurance billing type and payments paid by both the client and the insurance company.

To protect clinician and practice privacy, we only included rates in cities and states with a sufficient number of unique clinicians and appointments. Take a look at how each state compares to each other, along with select cities’ total payment prices.

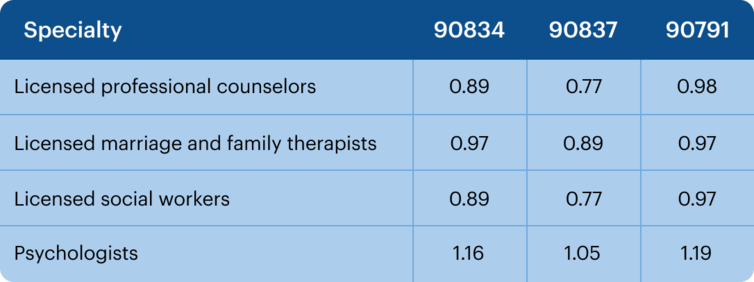

Table 1. Rate factors

N=2,196,977, Source: SimplePractice, 2021 CPT® Code Study

The chart above shows a few different specific factors, and what percent of the total median you should multiply, based on your license.

For example, if you’re a licensed professional counselor (LPC), and the median insurance reimbursement rate is $86 for CPT® code 90834 in your state, you would multiply:

$86 × 0.89 = $76.54

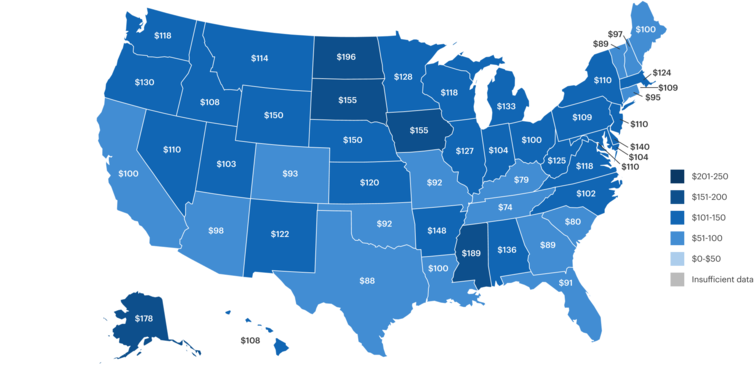

CPT® code 90791: Median total payment by state

N=2,196,977, Source: SimplePractice, 2021 CPT® Code Study

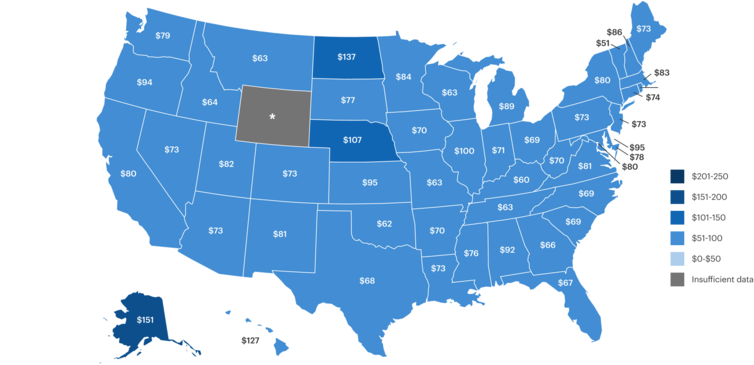

CPT® code 90834: Median total payment by state

N=2,196,977, Source: SimplePractice, 2021 CPT® Code Study

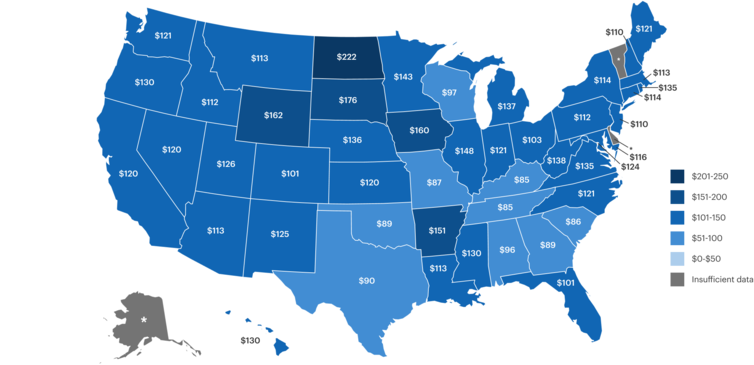

CPT® code 90837: Median total payment by state

N=2,196,977, Source: SimplePractice, 2021 CPT® Code Study

Insurance groups have come a long way in the past few years on how they value and treat mental health—but it doesn’t mean that there isn’t more that can be done. Insurance companies need to start including a wider range of mental health services that can be provided even under the most basic plans. This includes coverage for preventative care, along with more options for treatment. Aside from the health benefits this will provide to clients, it’ll make it easier for clinicians to be fairly paid for the critical work they’re doing.

While this study only evaluates a handful of CPT® codes and insurance scenarios, it’s safe to say that these can heavily influence and affect practitioners at any stage of their career.

It’s important to understand the basics of insurance in order to successfully accept it for your practice and still make a livable income.

SimplePractice is HIPAA-compliant practice management software with everything you need to run your practice built into the platform—from booking and scheduling to insurance and client billing.

If you’ve been considering switching to an EHR system, SimplePractice empowers you to streamline appointment bookings, reminders, and rescheduling and simplify the billing and coding process—so you get more time for the things that matter most to you.

Try SimplePractice free for 30 days. No credit card required.

2021 Methodology

The CPT® code data reflected in this article was based on 2.2 million appointments from 31,000 SimplePractice behavioral health customers from January 1st, 2021 through August 8th, 2021. This sample specifically filtered CPT® codes, billing type, and payments made by both clients and insurance.

All rights reserved. No part of this publication may be reproduced, distributed, or transmitted in any form or by any means without giving SimplePractice appropriate credit and link.

Proudly made in Santa Monica, CA © 2025 SimplePractice, LLC

Proudly made in Santa Monica, CA © 2025

SimplePractice, LLC